By Sinead Floody, 21st August 2017 (updated 03.07.2024)

The Companies Accounting Act 2017 (the 2017 Act) was signed into law on 9th June 2017, transposing Directive 2013/34/EU of the European Parliament into Irish law. The enactment of this legislation extends the definition of Unlimited Companies and introduces the new Micro Company.

Unlimited Companies

The 2017 Act eliminates the old exemption from filing accounts for Unlimited Companies with a non- EU/EEA shareholding structure comprising of limited liability. The scope for Unlimited Companies to avoid filing financial statements is much reduced as the 2017 Act has increased the scope of what is considered to be a “Designated Unlimited Company” – which is a company that is not exempt from filing financial statements. This, in turn, introduces the end of the possibility to have non-filing structures. Prior to the Companies Accounting Act 2017, an Unlimited Company that was owned by a non-EEA incorporated Unlimited Company did not fall under the definition of a Designated Unlimited Company; and therefore was not required to file financial statements each year with its annual return.

By the very nature of filing annual financial statements, comparative yearly figures will also have to be reported. The annual return is filed alongside the financial statements to the CRO, which is then, almost instantly, made available to the public.

All Unlimited Companies in Ireland are required to have the suffix “Unlimited Company” at the end of their company name, since the enactment of the Companies Act 2014 (the 2014 Act). The 2014 Act allowed an application to be made to the Minister of Jobs, Enterprise and Innovation to obtain an exemption from including this suffix in the company name. The 2017 Act has removed this exemption from the law, however, this will not have retrospective effect, meaning all current Unlimited Companies with an exemption will remain exempt.

Changes to Company Accounting Requirements

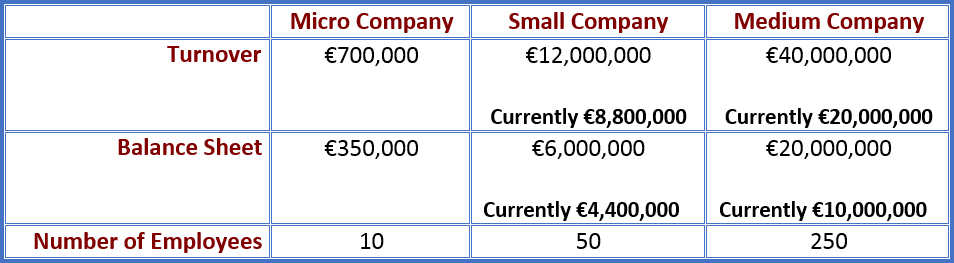

Alongside introducing changes to the threshold for small and medium companies, the 2017 Act introduces the “Micro Company” into company law and company accounting. This company type is only available to Private Companies and not to Public Limited Companies or Unlimited Companies. Some Private Companies such as investment companies, financial holding undertakings, subsidiaries that are included in consolidated financial statements or group structures, cannot avail of the Micro Company regime.

A company is considered to be a ‘Micro Company’ if their annual turnover does not exceed €700,000 and their balance sheet is under €350,000. Micro Companies are exempt from disclosing directors’ remuneration in their financial statements as well as being exempt from the requirement of filing a director’s report. The 2017 Act has increased the threshold for small and medium companies and is illustrated in the table below.

This threshold increase has broadened the scope for a company to claim audit exemption, however, medium companies will be required to file a full set of financial statements without any abridgement allowed. The 2017 Act also requires directors to disclose payments made by the company to any government agencies if the company’s activities involve mining, extraction or the logging of primary forests.

The Companies Registration Office has confirmed that changes to filing requirements are only applicable to financial years beginning on or after 1st January 2017.

As of July 2024, the EU has implemented the European Union (Adjustments of Size Criteria for Certain Companies and Groups) Regulations 2024, requiring all member states to increase the thresholds for company sizes by circa 25%. Read about the new Irish Company thresholds here.

Issues with the Companies Act 2014 is Addressed by the 2017 Act

The Companies Accounting Act 2017 clarifies the definition of “credit institution”, which was unclear in the 2014 Act. The 2014 Act also only offered merger relief to transactions involving two Irish companies. The 2017 Act provides relief to transactions where the acquired company is a body corporate, including those registered outside Ireland. The 2017 Act has also implemented the recommendations of the Company Law Review Group on the Belgard Motors case to avoid automatic crystallisation of floating charges.

Disclaimer This article is for guidance purposes only. It does not constitute legal or professional advice. No liability is accepted by Company Bureau for any action taken or not taken in reliance on the information set out in this article. Professional or legal advice should be obtained before taking or refraining from any action as a result of this article. Any and all information is subject to change.