By Sinead Floody, 16th Nov 2016 (updated 03.07.2024)

The Companies (Accounting) Bill 2016 (the Bill) has recently been published, which, if enacted, will give effect to Directive 2013/34/EU of the European Parliament and of the Council of 26th June 2013 on the annual financial statements of Irish Companies. The Bill also recommends some amendments to the Companies Act 2014 to correct problems arising thereof, which have been recognised since its enactment in June 2015, namely that a company which files its 6-month annual return late will not lose its audit exemption.

Non-Filing Entities

The Bill proposes to eliminate the current exemption from filing accounts for unlimited companies with a non-EU/EEA shareholding structure comprising limited liability. The scope for unlimited companies to avoid filing financial statements is much reduced. The Bill amends certain descriptions in this regard and refers to unlimited companies where the “ultimate beneficial owners enjoy the protection of limited liability”. Section 76 of the Bill brings more kinds of unlimited companies within the requirement to file audited financial statements on an annual basis.

It has not been formally stated when the Bill shall be enacted; however, companies that will be affected by these changes should bear in mind that the previous year’s figures will have to be included in the financial statements as comparator figures for the current year. Non-filing entities should identify how their company will be affected by publicly disclosing their financial statements and should discuss the same with their accountant or business advisers.

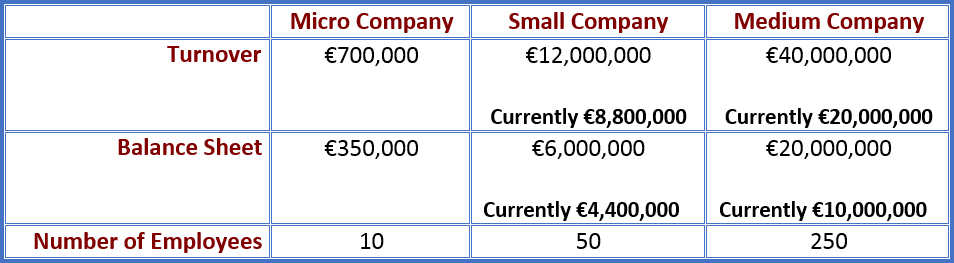

The ‘Micro Company’

The Bill will introduce a ‘micro companies’ regime, as well as implement changes to the current small and medium company thresholds. A company will be considered to be a ‘micro company’ if its annual turnover does not exceed €700,000 and the balance sheet is under €350,000. Micro companies will be exempt from disclosing directors’ remuneration in their financial statements, as well as being exempt from the requirement of filing a director’s report. Public Limited Companies and Unlimited Companies cannot avail of the benefits of the micro company regime. The Bill increases the threshold for small and medium companies and is illustrated in the table below.

This threshold increase will broaden the scope for a company to claim audit exemption, however medium companies will be required to file the full shareholders’ financial statement without any abridgment allowed. The Bill will also require directors to disclose payments made by the company to any government agencies if the company’s activities involve mining, extraction or the logging of primary forests.

As of July 2024, the EU has implemented the European Union (Adjustments of Size Criteria for Certain Companies and Groups) Regulations 2024, requiring all member states to increase the thresholds for company sizes by circa 25%. Read about the new Irish Company thresholds here.

Timing for the Companies (Accounting) Bill 2016

Although no time frame has been made available in relation to the legislative process surrounding enacting the Bill, it is assumed that this may not take much longer as Ireland was required to have transposed Directive 2013/34/EU of the European Parliament and of the Council of 26th June 2013 into our domestic legislation by 20th July 2015. We will be monitoring the progress of this Bill as goes through its final stages and will update this blog accordingly.